What is Life Insurance in India?

Life Insurance in India is one of the most important tools of financial planning. A life insurance policy ensures that your family members receive financial support in case of your untimely death. The insurance company pays a lump sum, called the death benefit, to your nominated beneficiaries. This amount can help them cover daily expenses, housing, children’s education, loan repayments, and even long-term goals.

Life insurance in India is not just about protection—it is also about planning for the future. Depending on the type of policy, it can offer both financial security and savings growth.

Basic life insurance coverage come in two varieties.

- Plans for Pure Protection

A pure protection plan is a kind of life insurance policy that, in the case of your untimely death, guarantees your family a sizable quantity of money with no maturity benefits. - Plans for savings and protection

A protection and savings plan is a dual benefit life insurance policy that provides both savings for long-term objectives like retirement or a child’s education as well as financial security.

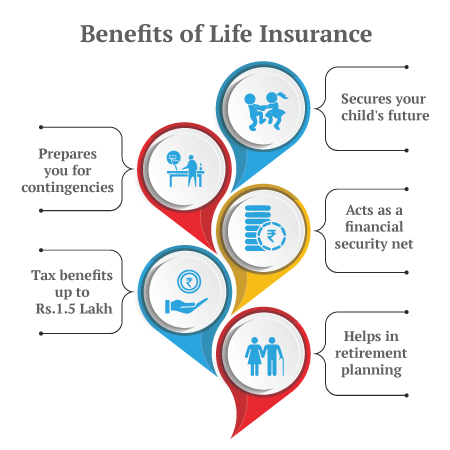

Benefits of Life Insurance in India

Financial Security

By paying out a lump sum in the event of the insured’s death, Life Insurance in India offers loved ones a financial safety net. This ensures that dependents may maintain their standard of living and fulfill vital expenses. The definition of life insurance emphasizes how it provides security against monetary instability brought on by unanticipated events.

Income Replacement

When the policyholder passes away, Life Insurance in India is primarily intended to replace lost income. This assists dependents with long-term financial objectives, mortgage repayment, and everyday spending management. The significance of life insurance goes beyond simple protection; it guarantees families’ financial stability.

Debt Settlement

A lot of people have bills from credit cards, personal loans, and home loans. Life insurance in India makes sure that remaining family members are not burdened by unpaid debts. A carefully thought-out life insurance policy protects assets and avoids financial strain.

Education and Future Planning

Life Insurance in India can assist in paying for a child’s schooling, marriage, or even the long-term goals of a family. By guaranteeing that future milestones are reached without encountering financial obstacles, it plays a vital role in financial planning. The meaning of life insurance encompasses both financial growth and protection.

Tax Benefits

Under sections 80C and 10(10D) of the Indian Income Tax Act, life insurance policies provide tax benefits. Policyholders can guarantee their loved ones’ financial stability while saving money on taxes. The definition of life insurance states that it is a useful financial instrument that provides both tax efficiency and protection.

Peace of Mind

It is quite reassuring to know that dependents are financially protected in the event of an unforeseen circumstance. A Life Insurance in India policy is a crucial component of prudent financial planning since it guarantees that families won’t face financial difficulties.

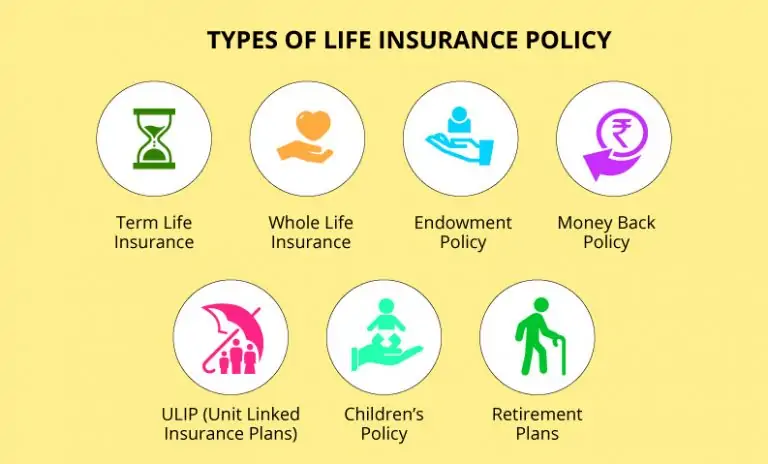

Types of Life Insurance Policies in India

Different types of life insurance policies are available to accommodate a range of financial objectives and tastes. These are the primary kinds.

Term Life Insurance in India

Term insurance offers protection for a predetermined time frame (such as ten or twenty years), during which a death benefit is paid if the policyholder dies. It doesn’t get worth more in cash.

Whole Life Insurance Plans in India

Provides lifetime protection, a death payout that is assured, and gradually builds up cash value. This cash value is available for policyholders to borrow against or withdraw from.

Universal life insurance

allows for flexible premium and death benefit payments while building up cash worth through interest. It permits coverage and premium modifications according to a person’s financial situation.

Variable life insurance

combines cash value that can be invested in sub-accounts such as equities and bonds with death benefits. Depending on how well an investment performs, returns can increase.

Endowment policies

After a predetermined period of time or upon the insured’s passing, endowment policies make a lump payment. It functions as insurance as well as a savings tool.

Unit Linked Insurance Plans (ULIP)

combines financial choices with life insurance. ULIPs give you the freedom to divide premiums among different funds (debt, equity) according to your financial objectives and risk tolerance. Returns are contingent on the performance of the fund, which offers insurance coverage and growth potential. A ULIP calculator will assist you in determining the maturity value of a ULIP based on factors such as fund selection, tenure, and premium if you intend to invest in one.

Child plans

Child plans are made especially to cover a child’s future tuition and living expenses in the event that the policyholder passes away. At significant turning points in the child’s life, it offers financial help.

Money-back plans

In addition to the death benefit, provide recurring payments (survival benefits) throughout the duration of the policy. It meets financial needs by supplying liquidity on a regular basis.

Retirement plans

Intended to guarantee financial independence by offering a consistent income after retirement. It allows policyholders to keep their way of life after retirement by providing either a lump sum or regular payments (an annuity).

Why Buy Life Insurance in India?

Life Insurance in India is more than just a policy—it’s a commitment to your family’s well-being. With rising expenses, uncertain health conditions, and growing financial responsibilities, buying life insurance early ensures affordable premiums and maximum coverage.